US Dollar Index gathers traction and tests 93.40

- DXY picks up pace and adds to Friday’s gains near 93.40.

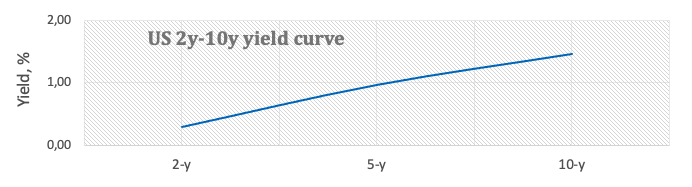

- US 10-year yields pushes higher and approaches 1.47%.

- Fedspeak, Durable Goods Orders, Dallas Fed Index next on tap.

The greenback, when tracked by the US Dollar Index (DXY), starts the week on the same upbeat mood that finished the last one and re-visits the 9240/50 band on Monday.

US Dollar Index looks to data, Fedspeak, yields

The index advances for the second session in a row on Monday and approaches the 93.50 area on the back of higher yields and broad-based softer note in the risk-associated universe.

Indeed, yields of the US 10-year benchmark note pushe higher and gyrate around the 1.47% level, area last traded in late June. In the short-end of the curve, yields of the 2-year note climb to the 0.28% zone, last observed in April 2020.

Furthermore, the renewed and moderate pick-up in US yields follow the hawkish tone from Chief Powell at the latest FOMC event (Wednesday). In the same line, Cleveland Fed L.Mester (2022 voter, hawkish) advocated on Friday for the start of the tapering process in November and finish in mid-2022.

Later in the US data space, Durable Goods Orders for the month of August are due seconded by the Dallas Fed Manufacturing Index. In addition, speeches by NY Fed J.Williams (permanent voter, centrist), FOMC Governor L.Brainard (permanent voter, dovish) and Chicago Fed C.Evans (voter, centrist) will also be iin the limelight throughout the session.

What to look for around USD

The index flirts with recent tops in the 93.40/50 band, always with the attention on higher yields. The improved mood in the buck follows the unexpected hawkish message from Chief Powell while market participants continue to pencil in an interest rate hike by end of 2022. Positive results from US fundamentals coupled with alleviating concerns regarding the progress of the Delta variant should also remain supportive of a stronger dollar in the near/medium term.

Key events in the US this week: Durable Goods Orders (Monday) – Advanced Goods Trade Balance, CB Consumer Confidence, Powell’s Testimony (Tuesday) – Powell’s speech (Wednesday) – Final Q2 GDP, Initial Claims (Thursday) – PCE, Final Manufacturing PMI, ISM Manufacturing, Personal Income/Spending, final Consumer Sentiment (Friday).

Eminent issues on the back boiler: Biden’s multi-trillion plan to support infrastructure and families. US-China trade conflict under the Biden’s administration. Tapering speculation vs. economic recovery. Debt ceiling debate. Geopolitical risks stemming from Afghanistan.

US Dollar Index relevant levels

Now, the index is gaining 0.17% at 93.43 and a break above 93.52 (monthly high Sep.23) would open the door to 93.72 (2021 high Aug.20) and then 94.30 (monthly high Nov.4 2020). On the flip side, the next down barrier emerges at 92.98 (weekly low Sep.23) seconded by 92.73 (55-day SMA) and finally 91.94 (monthly Sep.3).